Founder's Note

Stablecoins have quietly become a consequential development in digital finance since Bitcoin’s inception. What began as a liquidity tool for crypto markets has evolved into the infrastructure layer for global payments, cross-border settlements, and institutional treasury management.

The shift is structural, not speculative. As central banks test digital currencies and major financial intermediaries (banks, brokers, and payment platforms) integrate stablecoin rails, we are witnessing the convergence of crypto architecture with the regulated financial system. For example, Morgan Stanley’s recent move to introduce retail crypto trading through E*TRADE signals that digital assets are entering the same compliance, taxation, and audit frameworks as traditional instruments.

For businesses and investors, the implications are tangible:

- Tax and accounting treatment of stablecoin holdings and transactions may vary per country unless a consistent, unified treatment is laid out.

- Regulatory classification and licensing under national regimes are now taking shape across the EU, UK, UAE, and US.

- Reserve management and auditability, increasingly subject to disclosure and prudential oversight.

- Compliance obligations (AML, reporting, and contractual standards) aligning with mainstream financial norms.

At Noema, our approach remains technology-neutral and compliance-first. We see stablecoins not as a speculative trend but as a bridge between innovation and institutional accountability. Our focus is to help clients navigate jurisdictional nuance around permissibility and enforcement, interpret evolving reserve and redemption rules, and anticipate how regulators will translate these frameworks into enforcement.

In this edition of our Client Newsletter, our team maps key developments across major markets and provides a concise glossary to demystify terms shaping the industry, as stablecoins move from the margins of crypto into the machinery of global finance.

Onwards,

Giammarco Cottani

Founding Partner, Noema Global

Key Market Developments

- Brokerage rails: Morgan Stanley’s E*TRADE has announced crypto trading via a partner (early 2026 target)—traditional brokers are converging with digital assets.

- Payments pilots: Singapore stablecoin payments are moving into mainstream retail integrations (GrabPay ecosystem).

- Non-USD pegs on the rise: From AED exploration to offshore CNY and KZT pilots, FX diversity in stablecoins is accelerating.

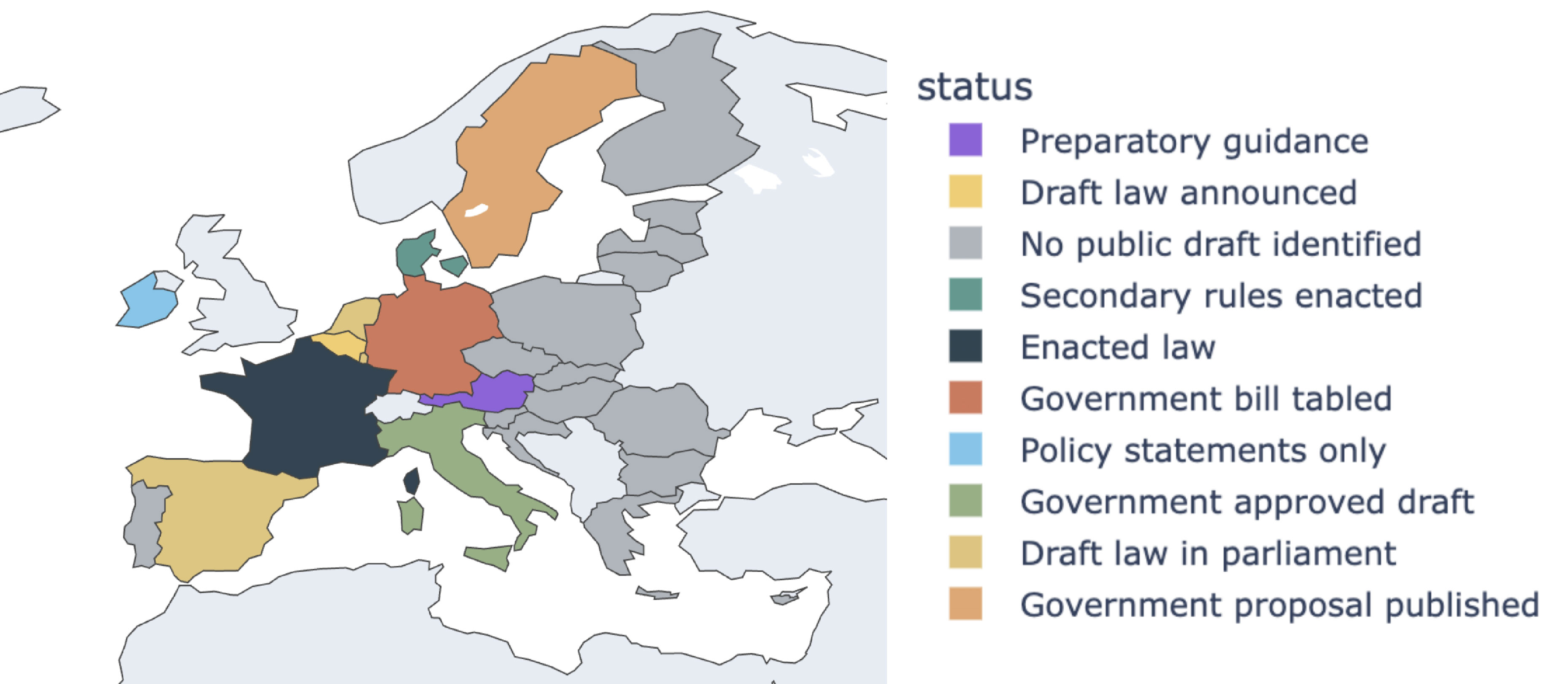

Policy and Market Mapping

United States

Federal stablecoin bills are active (2025 STABLE Act introduced); rulemaking posture evolving across banking/markets regulators. Meanwhile, brokerages/banks are expanding digital-asset access (E*TRADE crypto trading announced for 2026 via a regulated partner). Bank-like standards for payment stablecoins (reserve quality, supervision) are expected. U.S. issuers or distributors, should budget for prudential-style compliance and state overlays pending federal pre-emption.

EU

The EU has passed a major law (MiCA) that sets out rules for stablecoins. Coins pegged to the euro or to a basket of assets must be licensed, backed by high-quality reserves, and redeemable on demand. This is the most comprehensive framework so far and will likely influence global standards. Firms operating in Europe will need EU-based reserves and strict compliance with disclosure and reporting.

Despite the 1 January 2026 deadline for transposing the DAC8 directive on crypto disclosure into domestic law is nearby, EU member states have been slow to propose their domestic legislation. While it is not unusual that transposition deadlines are not met, this does increase uncertainty for both businesses consumer.

United Kingdom

The UK is building a new regime for pound-pegged stablecoins, with oversight from the Financial Conduct Authority (FCA) and the Bank of England. Final rules expected in 2026. London is a global finance hub, so its approach could shape wider markets. Issuers and custodians will face authorization requirements and reserve quality checks, much like e-money.

Singapore

The Monetary Authority of Singapore (MAS) finalised a stablecoin framework applying to single-currency stablecoins (SCS) pegged to SGD or G10; branding as “MAS-regulated stablecoin” requires strict reserve, redemption (T+5), capital, governance tests. Industry is piloting retail payments on stablecoin rails. For SGD/G10 issuers, Singapore offers regulatory certainty and brand value, and unsurprisingly, compliance is demanding (onshore issuer, audits, daily reconciliation). Merchants may see lower acceptance costs via stablecoin-to-fiat conversion stacks.

Japan

Since June 2023, amended Payment Services Act (FSA Weekly Review no. 642)allows issuance via licensed banks, trust banks, and money transfer firms, with strict redeemability and reserve controls; further refinements continue through 2024–25. First major economy with a comprehensive, redeemability-first law—template for safety-led regimes. If issuing/servicing in Japan, expect bank-proximate structures; foreign models often need local trust/bank partners and J-GAAP reserve treatment.

Hong Kong

Stablecoins Ordinance passed May 2025; as of 1 Aug 2025, issuing fiat-referenced stablecoins requires an HKMA licence (governance, reserves, redemption, disclosure). Hong Kong and Singapore are competing to be Asia’s digital asset hubs. To operate in Hong Kong, companies must plan for HKMA licensing and high governance standards.

United Arab Emirates

The UAE’s central bank finalized rules in 2024 for dirham-pegged stablecoins and certain foreign tokens. Algorithmic stablecoins are banned. Merchants will only be allowed to accept AED-pegged stablecoins for goods and services. UAE is emerging as a stablecoin payments hub (and even exploring AED-pegged products from private issuers). Companies doing business in the Gulf may need to design AED-based solutions to comply (or compliant foreign tokens for specific uses). Expect licensing/registration, marketing restrictions, and coordination with ADGM/VARA/DFSA where relevant.

Further, the UAE has taken a significant step toward enhancing global tax transparency in the crypto sector by signing the Multilateral Competent Authority Agreement on the Automatic Exchange of Information under the Crypto-Asset Reporting Framework (CARF) on September 20, 2025. This agreement, building on the UAE's commitment announced last November, establishes a standardized mechanism for the automatic exchange of tax-related information on crypto activities, providing much-needed certainty and clarity for stakeholders including advisory providers, intermediaries, traders, custodians, and exchange platforms. With implementation set to go live in 2027 and the first information exchanges in 2028, CARF aligns the UAE with international standards to combat tax evasion while fostering a compliant and innovative digital asset ecosystem. In response, we at Noema Global will be actively participating in the ongoing public consultation, launched on September 15 and open until November 8, 2025, to help shape effective regulatory rules—we invite our clients to join us by sharing their insights and recommendations.

Kazakhstan

Tenge-pegged stablecoin pilot launched within the central bank’s regulatory sandbox (local bank/exchange + Solana/Mastercard partners). Separately, offshore yuan-linked stablecoin (AxCNH) launched in Kazakhstan after local approval. Illustrates non-dollar stablecoins are gaining traction, especially in cross-border trade. Clients trading in Central Asia will need to watch on/off-ramp rules, KYC, and potential FX controls; treasury teams may pilot non-USD liquidity but must model convertibility & counterparty risk.

Key Terms

- Cryptocurrency: Digital currency, purely based online with no physical form, and is recorded on a public digital ledger called a blockchain, which is maintained by a network of computers. It relies on cryptography both to protect transactions and to regulate the creation of new units. Unlike traditional money, it does not rely on banks or a central government, and it has no legal tender status, meaning no one is obliged to accept it as payment. Its price is determined only by supply and demand.

- Cryptography1: The techniques and mathematical systems used to secure digital information and verify transactions. It ensures that data can be exchanged privately and cannot be altered, accessed, or forged without authorization. In the context of digital assets, cryptography underpins secure, tamper-resistant transactions without relying on a central intermediary.

- Distributed Ledger (“DL”)2: a shared record-keeping system where data is stored, updated, and verified across multiple computers rather than a single central database. This decentralised structure enhances transparency, security, and resilience. Blockchain is the most widely known form of distributed ledger technology (DLT).

- Blockchain3: a decentralised (distributed) digital ledger that records transactions across multiple participants’ systems and links data in time-ordered “blocks” secured via cryptographic methods. This makes the record hard to change and helps build trust without a central authority.

- Distributed Ledger Technology (“DLT”)4: is a means of recording information through a distributed ledger. These technologies enable nodes (i.e. computers) in a network to propose, validate, and record state changes consistently across the network's nodes – without relying on a central trusted party.

- Stablecoin: A digital token pegged to a real-world currency, designed to keep its value stable.

- Fiat-backed stablecoin: Backed by cash or government bonds held in reserve (e.g., USD Coin).

- Asset-referenced token (EU term): A coin tied to more than one asset (e.g., a mix of currencies or commodities).

- Algorithmic stablecoin: Tries to keep its peg using computer code and incentives rather than reserves. Many regulators ban these.

- Redeemability: The right to swap your stablecoin back into traditional money at face value.

- Reserves: The assets (cash, short-term government bonds) that back each stablecoin.

- Tokenised deposit: A bank deposit recorded on a blockchain instead of a bank ledger. Competes with stablecoins.

- CBDC (Central Bank Digital Currency): A digital version of a country’s currency, issued directly by the central bank.

- On/Off-ramp: The process of exchanging between crypto assets and traditional money.

- Travel Rule: A global rule requiring crypto transactions to include sender and recipient information, to prevent money laundering.